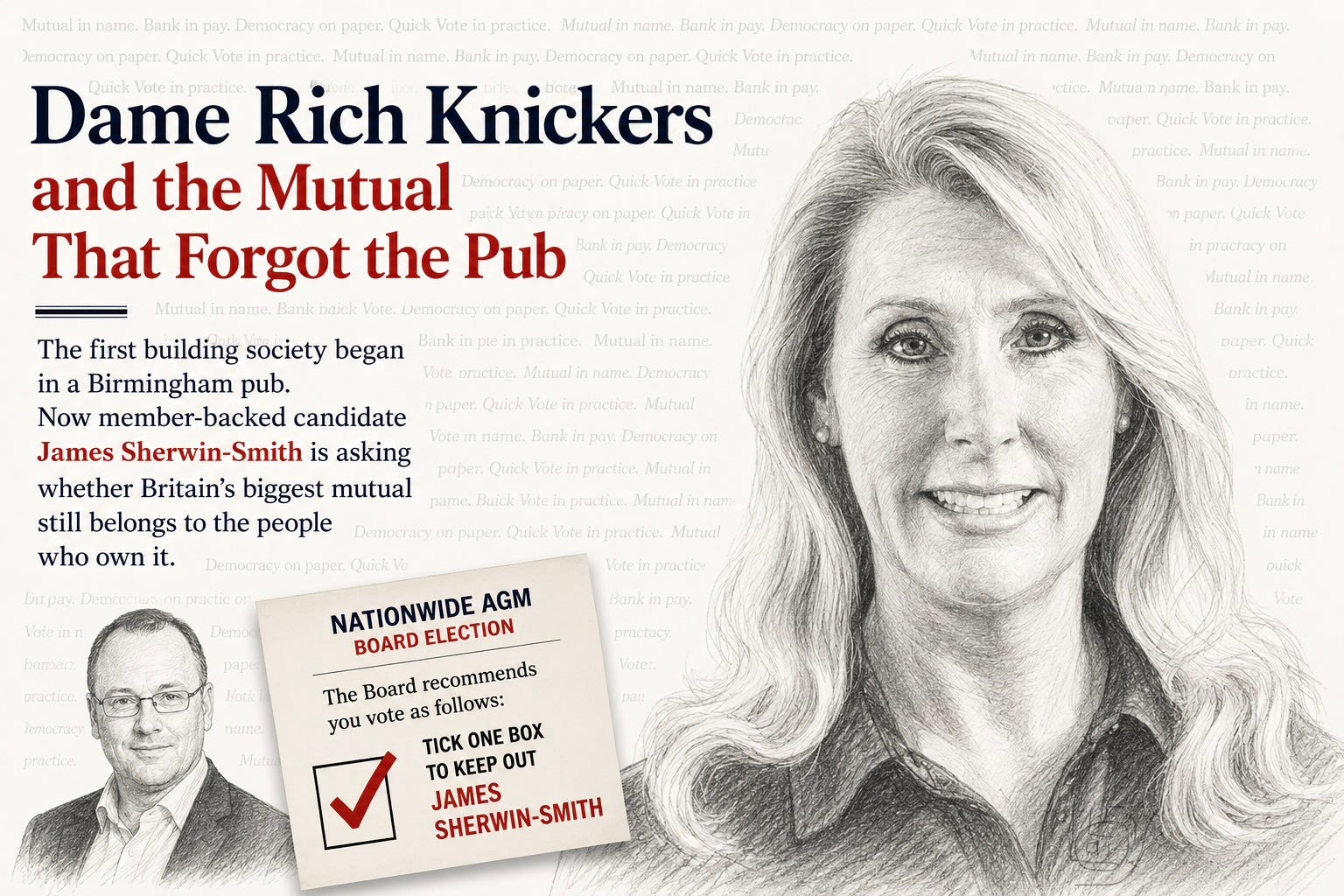

Dame Rich Knickers and the Mutual That Forgot the Pub

The first building society began in a Birmingham pub. Now member-backed candidate James Sherwin-Smith is asking whether Britain’s biggest mutual still belongs to the people who own it.

By Mike Olley

Jun 22, 2026

Link: https://www.midlandsgrit.co.uk/p/dame-rich-knickers-and-the-mutual

The building society movement began in Birmingham. Not in a glass tower. Not in a shareholder presentation. Not in a strategy away-day where somebody in expensive trainers wrote “member journey” on a flip chart and charged £8,000 for the privilege. It began in a pub. In 1775, Richard Ketley founded what is generally regarded as the first building society at the Golden Cross Inn on Snow Hill. The idea was beautifully simple. Ordinary people pooled their money so ordinary people could build or buy homes. Neighbours helping neighbours. Mutual self-help. Birmingham at its practical best, before anyone had thought to ruin it with a remuneration committee.

Two hundred and fifty years later we arrive at Nationwide Building Society and a debate over a chief executive package worth about £4.7 million. Dame Debbie Crosbie, Nationwide’s chief executive, has attracted attention not because her package is huge by global banking standards, but because Nationwide keeps telling us it is not a bank. That is the whole pitch. The adverts say it. The branding says it. The mutual language says it. Nationwide is different. It belongs to its members. It is not one of those nasty shareholder banks with their bonuses, their boardrooms and their faint whiff of polished mahogany and moral escape tunnel.

And yet here we are, with members being asked to vote on a remuneration report that most ordinary people will never properly read and even fewer will fully understand. The details are available, of course. Nobody is suggesting they have been buried under the patio. But in the real world, if a member wants to understand what the chief executive is being paid, why she is being paid it, how much is salary, how much is bonus, how much is long-term incentive and what all this says about the soul of mutuality, they need time, patience, strong tea and perhaps a relative who once worked in pensions.

To be fair to Nationwide, there is a sensible argument. It is now a vast financial institution, made larger still by the acquisition of Virgin Money. It operates in a difficult, heavily regulated and competitive market. If you want serious people to run serious organisations, you may have to pay serious money. Compared with Wall Street, Dame Debbie’s package is not especially startling. Jamie Dimon at JPMorgan would probably regard £4.7 million as the sort of loose change one discovers in the lining of a winter coat. Some US bank chiefs earn sums so large they should arrive with oxygen and a warning from the Bank of England.

But that is not the right comparison, is it? Nationwide is not Goldman Sachs. It is not JPMorgan. It is not a listed bank owned by shareholders chasing dividends. If it wants to sell itself as a mutual, then members are entitled to compare it with mutuals, co-operatives and credit-union-style institutions. In America, large credit unions can certainly pay their chief executives well. Some pay hundreds of thousands of dollars. Some pay low millions. Very large ones can go higher. But even then, a £4.7 million package begins to look rather shiny for an organisation that still wants us to believe it has one foot in the old world of mutual self-help.

That is the real issue. Not whether Dame Debbie is clever. Not whether she works hard. Not whether Nationwide needs competent leadership. Of course it does. The question is what extra mutual benefit members receive in return. Better savings rates? Better mortgage rates? Better branch service? Stronger member democracy? Clearer accountability? A more powerful voice for the people who technically own the place? Because if the answer is simply that Nationwide has to pay like a bank because it has become very like a bank, then the obvious follow-up question is what remains meaningfully mutual apart from the marketing.

This is where the democracy becomes fascinating. Nationwide members are invited to vote. Splendid. Very mutual. Very wholesome. But then the voting papers present something called a Quick Vote. The Board recommends voting for items one to thirteen and against item fourteen. Tick one convenient box and your vote follows the Board’s recommendation across the board. Democracy has rarely been made so efficient. Whether it has been made better is another question. It is a little like being offered a restaurant menu where the waiter says, “You may choose anything you like, sir, but chef strongly recommends you have what chef has already chosen.”

I remember watching one of Birmingham’s old Co-operative societies conduct its democratic affairs. Officially, members elected directors. In practice, the names favoured by the leadership somehow always seemed to float to the top. Managers, who were also voting members, would quietly encourage staff, also voting members, to support particular candidates and, remarkably enough, those candidates usually won. It was democracy in much the same way Aston Villa are free to field eleven goalkeepers if they wish. Technically possible. Unlikely in practice.

I am not saying Nationwide is doing that. The circumstances are different and the organisation is much larger. But the memory came back because member organisations often face the same problem. The structure may be democratic, but most members are busy living their lives. They have jobs, mortgages, children, shopping, elderly parents and bins that may or may not be collected depending on where they live and which municipal tragedy is currently unfolding. They are not sitting at home with a highlighter pen studying board elections and remuneration reports. So the professionals take over, the machinery grows, the papers thicken and the member becomes less an owner than a warmly addressed spectator.

Item fourteen makes the point beautifully. It concerns James Sherwin-Smith, a member-nominated candidate seeking election to the Nationwide Board. He is not some wild-eyed revolutionary with a sandwich board and a megaphone. He has worked in financial services for more than twenty years. He has executive experience, board experience and a serious professional background. He gathered the required nominations from members and reached the ballot, which in itself appears to be a rare achievement. Nationwide’s Board recommends that members vote against him, arguing in effect that he does not have the right experience for an organisation of Nationwide’s scale and complexity.

Fair enough. The Board is entitled to its view. But members are entitled to notice the pattern. The Board-backed route appears smooth. The member-nominated route requires signatures, persistence, paperwork, scrutiny and then, if you finally arrive on the ballot, the Board tells the members not to vote for you. Again, this may all be perfectly proper. But it does raise the old mutual question: who really owns the society, the members or the people already running it?

And that brings us back to Richard Ketley, Birmingham and the Golden Cross Inn. No one appears to know what Ketley paid himself, but I think we can safely assume he was not trousering a modern long-term incentive plan while explaining performance gateways to a room of mildly baffled ale drinkers. The first building society was not born so executives could be benchmarked against banks. It was born because ordinary people needed homes and discovered they could achieve more together than alone.

Nationwide may be legally and commercially right to pay Dame Debbie what it pays her. Members may decide they are perfectly relaxed about it. They may also decide the Board is right about James Sherwin-Smith. That is democracy. But let us not pretend there is no question here. If members are being asked to endorse bank-style rewards, they are entitled to ask for mutual-style answers.

Two hundred and fifty years after a Birmingham pub helped launch the movement, the debate is no longer simply whether ordinary people can afford a house. It is whether ordinary people can still meaningfully influence the institutions they supposedly own. Richard Ketley might have understood that question perfectly. Then again, Richard Ketley never had consultants.