Why is Member financial benefit falling at Nationwide? Is the Fairer Share to blame?

Two topics often dominate conversations with Nationwide Members:

- The interest rate they pay / receive on the products they hold

- The £100 Fairer Share – did they get it – and more often than not, why didn’t they get it?

They are both closely related.

As a customer of a mutual, Members rightly expect to get a better rate on their products, as there is no need to generate profits to pay dividends to shareholders. But many are disappointed that Nationwide rarely tops the best buy tables, despite this structural advantage. Rather than being a price leader, Nationwide prices for value – and arguably offers a better overall proposition – better service, more branches etc.

The rationale for paying the Fairer Share – a dividend of sorts – to a minority of the Members is harder to explain. Nationwide is incentivising greater current account ownership and usage, that much is clear, and Nationwide is underweight in current accounts relative to its High Street competitors. But the arbitrary choice of the £100 figure which means it is not ad valorem, plus the post hoc setting of the eligibility rules, grates with many.

What is “Member financial benefit” vs “Member value”?

“Member financial benefit” is a historical measure that was first referenced in the 2017 Annual Report.

It’s currently defined as this: (see page 34, 2026 Annual Report)

Member financial benefit is calculated by comparing, in aggregate, Nationwide’s average interest rates and incentives to the market, predominantly using market data provided by the Bank of England and CACI, alongside internal calculations. The value for individual members will depend on their circumstances and product choices.”

Since the addition of the Fairer Share and the one off Big Thank you payments, Nationwide now also reports a “Member value” figure

Member financial benefit + these extras (paid to a subset of the members) = Member value

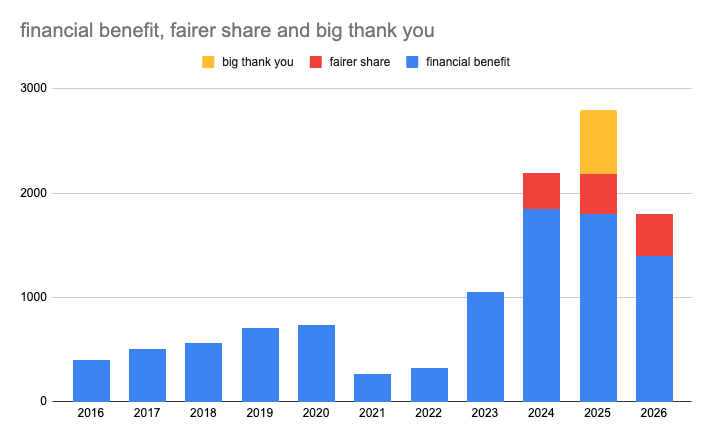

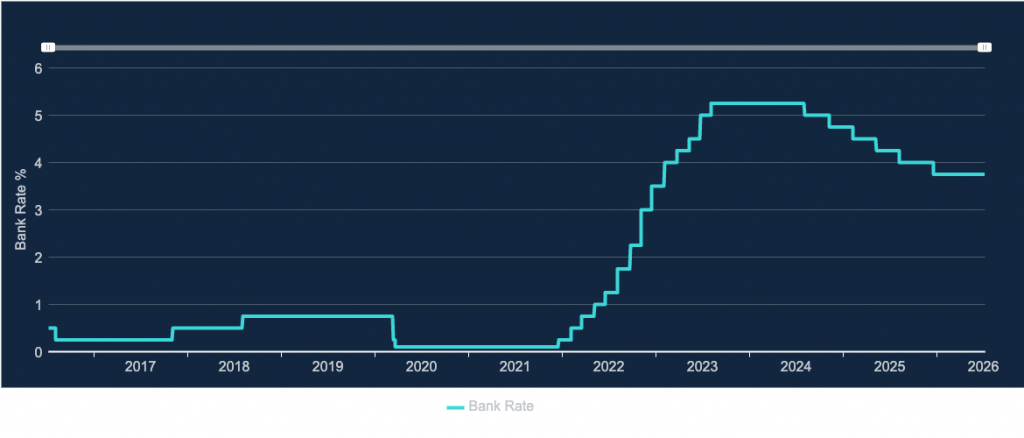

The below chart shows how the component parts of Member value have evolved over time. Note how the shape of Nationwide Member value closely correlates to the Bank of England bank rate over the same 10 year period.

Nationwide member value (2016-26)

Bank of England bank rate (2016-26)

When you strip back to the financial benefit, available to all members, you can see that not only is Member value down by £1BN in 2026, the underlying Member financial benefit is declining also.

But the falling financial benefit is not simply due to a falling bank rate. According to the Nationwide CFO, Muir Mathieson, (p32, 2026 Annual Report):

Member financial benefit decreased to £1.4 billion (2025: £1.8 billion) due to a narrowing of our mortgage and deposit customer rate differentials to the market in a lower Bank of England interest rate environment. Our average member deposit rates were 58 basis points (2025: 72 basis points) higher than the market average over the year.

i.e. in aggregate, Nationwide is pricing such that members are getting a worse deal on rates than last year, relative to the base rate.

The key point is this – while Member value appears to be tracking with bank rate, Member financial benefit is in decline relative to bank rate, as referenced by the CFO above. There is a clear substitution effect at work – Nationwide is paying out less in financial benefits in favour of the Fairer Share payment – which is only paid to a minority of Members.

While the member financial benefit figure has always been a relatively abstract number as it is only ever disclosed in aggregate, and the detailed calculation isn’t transparently shared, it was a good measure of pricing advantage. And while “the value for individual members will depend on their circumstances and product choices” the Fairer Share payments are distorting the distribution of the financial benefits even further with the ad valorem payments to a minority of members.

My personal view is that Members should have more say in how Nationwide chooses to accrue, and spend, profits that would otherwise become Member equity / reserves.

The last time there was a Member vote on a topic like this was 2007 – when Members were asked whether they supported 1% of the society’s profits being donated to charity (the “PerCent standard”).

Under the “Fairer Share” banner, Nationwide paid out c. £440M this year (more that 25% of pre-tax profits this year), and has paid out similar amounts in the preceding 3 years. But there was no vote on this new direction to delivering value to Members.

Data: https://docs.google.com/spreadsheets/d/1I4Bcp2hEze4GiJCEWiVbZzx3LAz-2xRaOnrx6mFIFVg/edit?usp=sharing